1

/

15

Perpetuals.com Ltd (NASDAQ: PDC)

Clene Inc., (NASDAQ: CLNN)

NioCorp Developments, Ltd. (NASDAQ: NB)

First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (FSE: KD0)

U.S. Gold Corp. (NASDAQ: USAU)

U.S. Energy Corporation (NASDAQ: USEG)

Phoenix Energy Services Corp. (OTCQB: PHXHF) (TSE: PHX)

First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (FSE: KD0)

Mawson Infrastructure Group, Inc. (NASDAQ: MIGI)

Jaguar Health, Inc. (NASDAQ: JAGX)

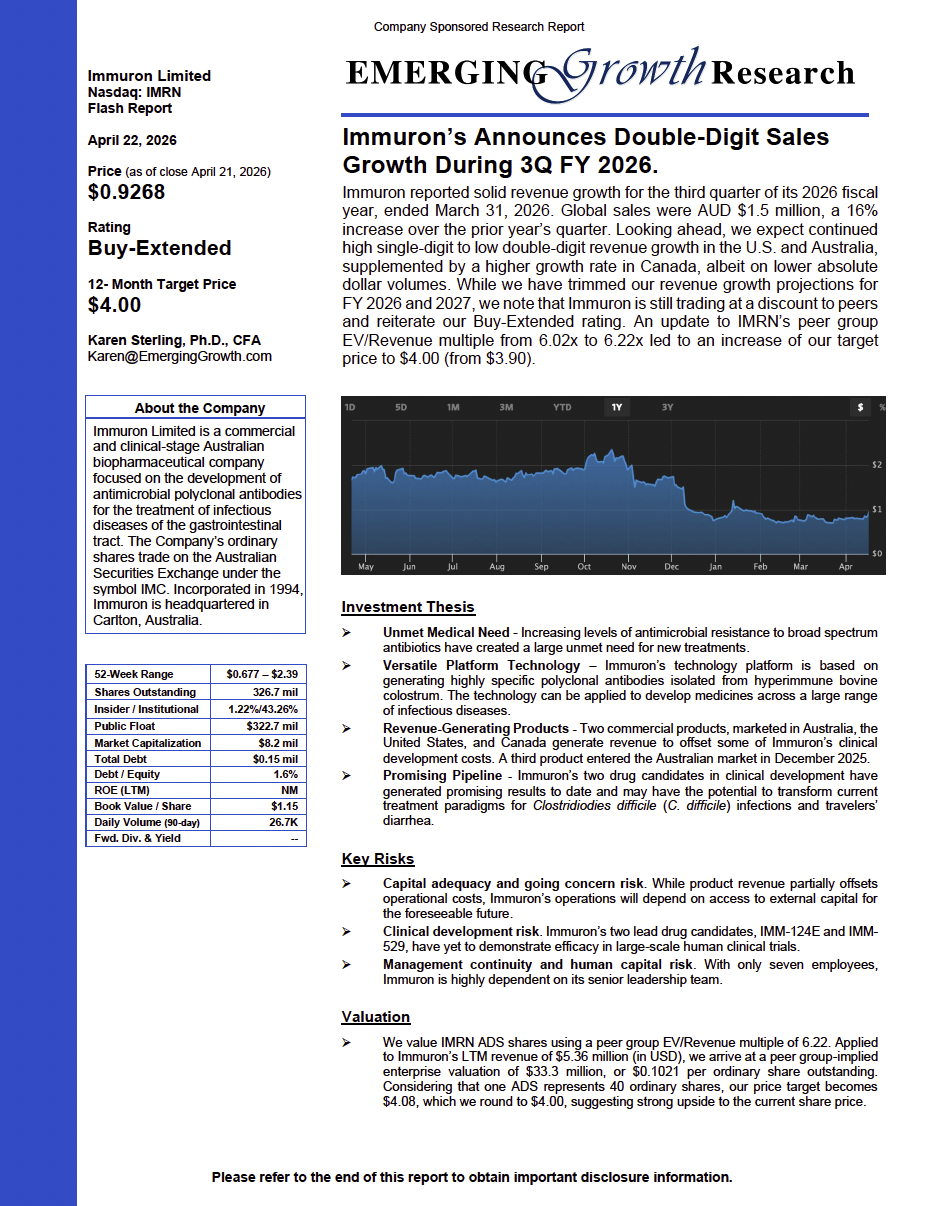

Immuron Limited (NASDAQ: IMRN)

Nova Minerals Limited (NASDAQ: NVA) (ASX: NVA)

1

/

15

Emerging Growth Company News

ZenaTech (NASDAQ: ZENA) Reports Record 558%...

Total assets grew 188% to $99.8 million; DaaS segment delivered over $10 million in first full year of operations Miami, FL–(Emerging Growth Newswire – April 29, 2026) – EmergingGrowth.com, a leading independent small cap media portal with an extensive history of providing unparalleled content for the...

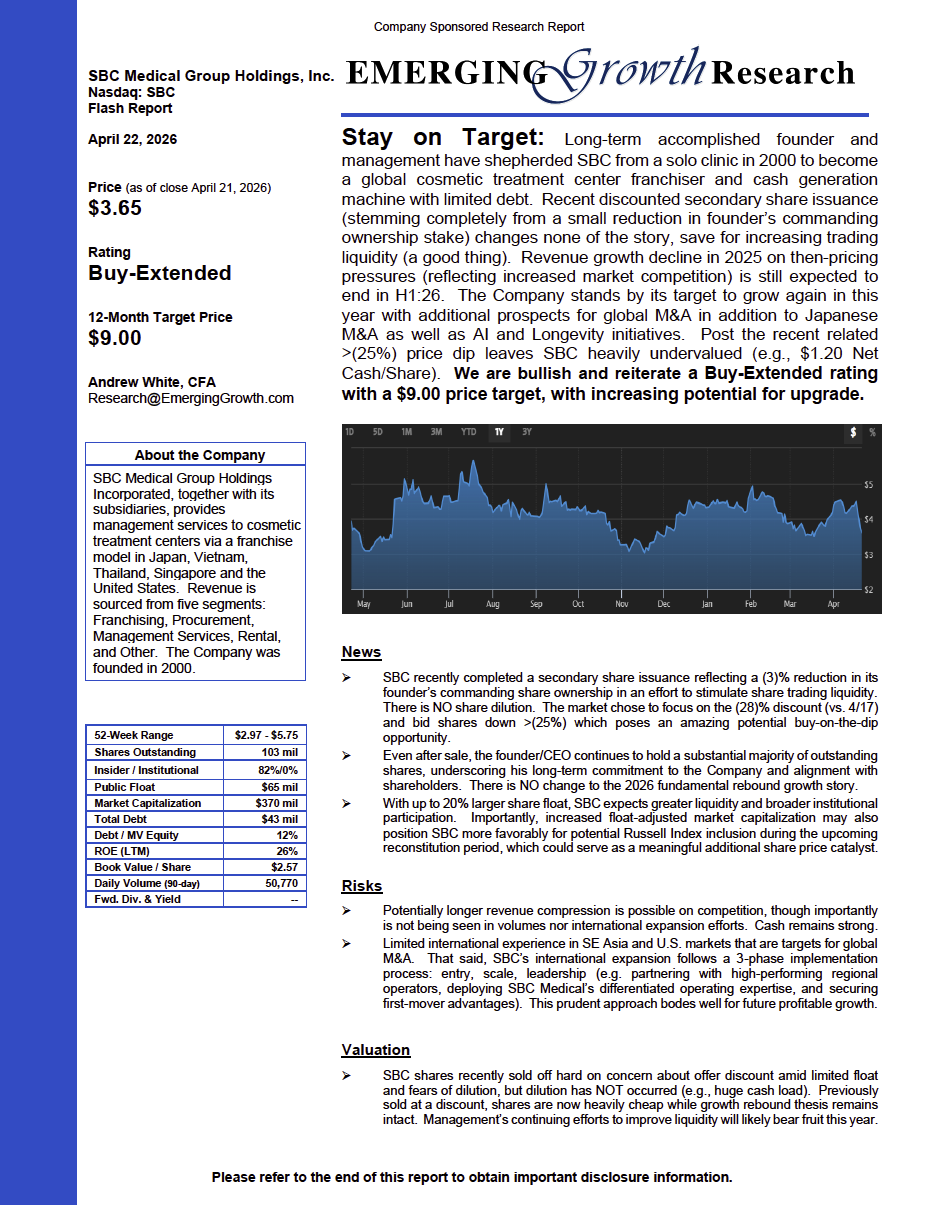

SBC Medical Group Holdings, Inc. (NASDAQ:...

Stay on Target: Long-term accomplished founder and management...

First Phosphate Corp. (OTCQX: FRSPF) (CSE:...

First Phosphate Completes Drill Programme First Phosphate (PHOS) has...

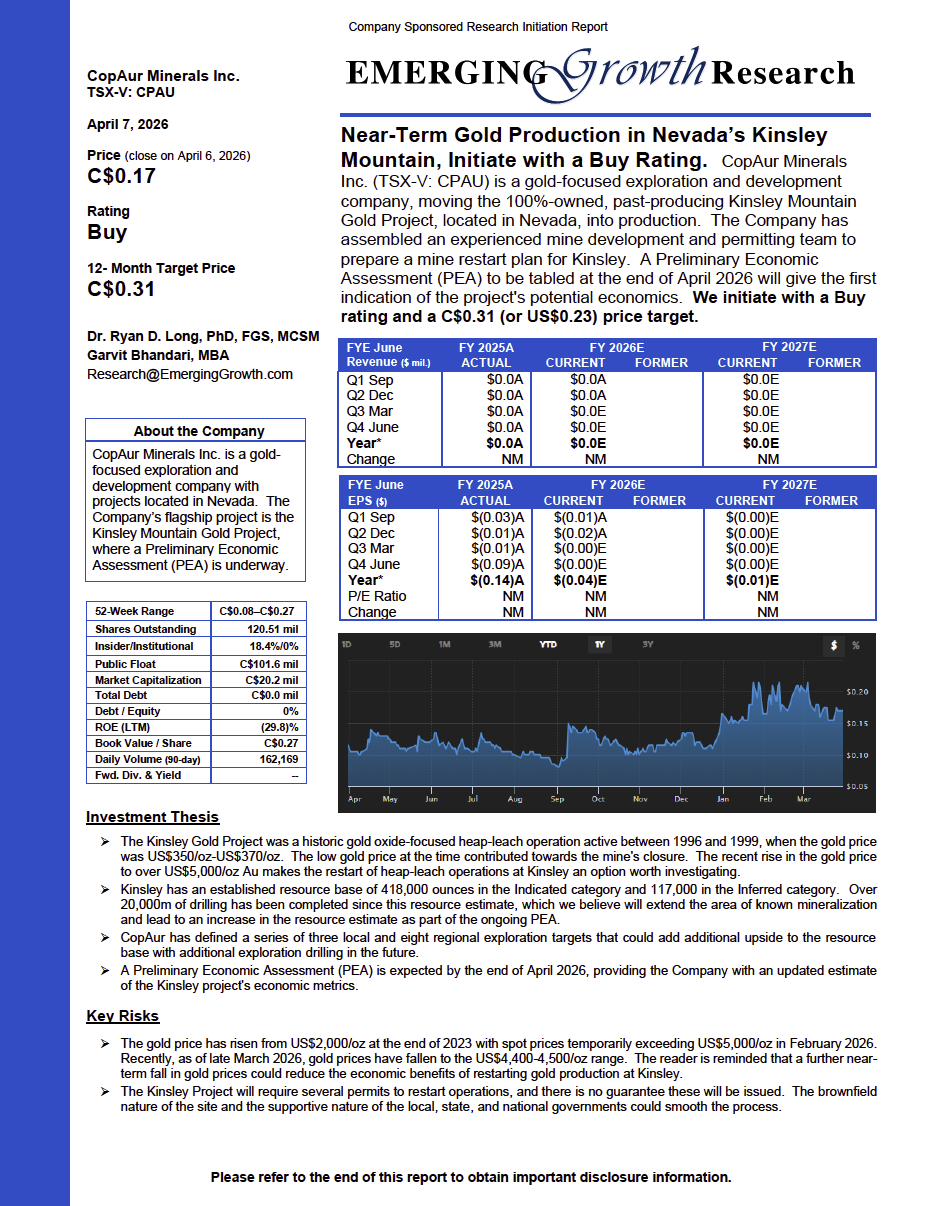

CopAur Minerals Inc. (TSXV: CPAU) (OTCQB:...

Near-Term Gold Production in Nevada’s Kinsley Mountain, Initiate...

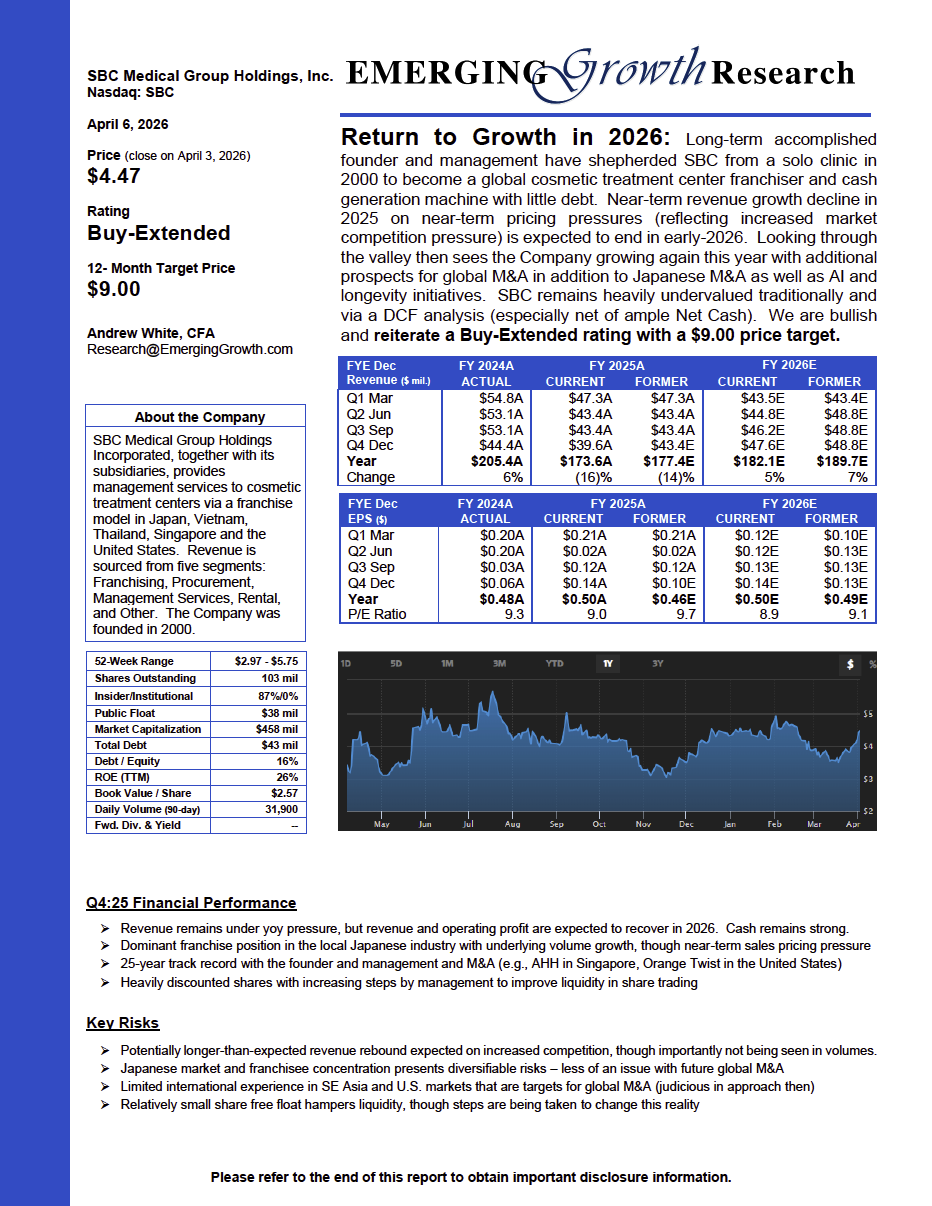

SBC Medical Group Holdings, Inc. (NASDAQ: SBC) Emerging Growth Research Report – April 6, 2026

Return to Growth in 2026: Long-term accomplished founder and management have shepherded SBC from a solo clinic in 2000 to become a global cosmetic treatment center franchiser and cash generation machine with little debt. Near-term revenue growth decline in 2025 on near-term pricing pressures (reflecting increased market competition pressure) is expected to end in early-2026. Looking through the valley then sees the Company growing again this year with additional prospects for global M&A in addition to Japanese M&A as well as AI and longevity initiatives.

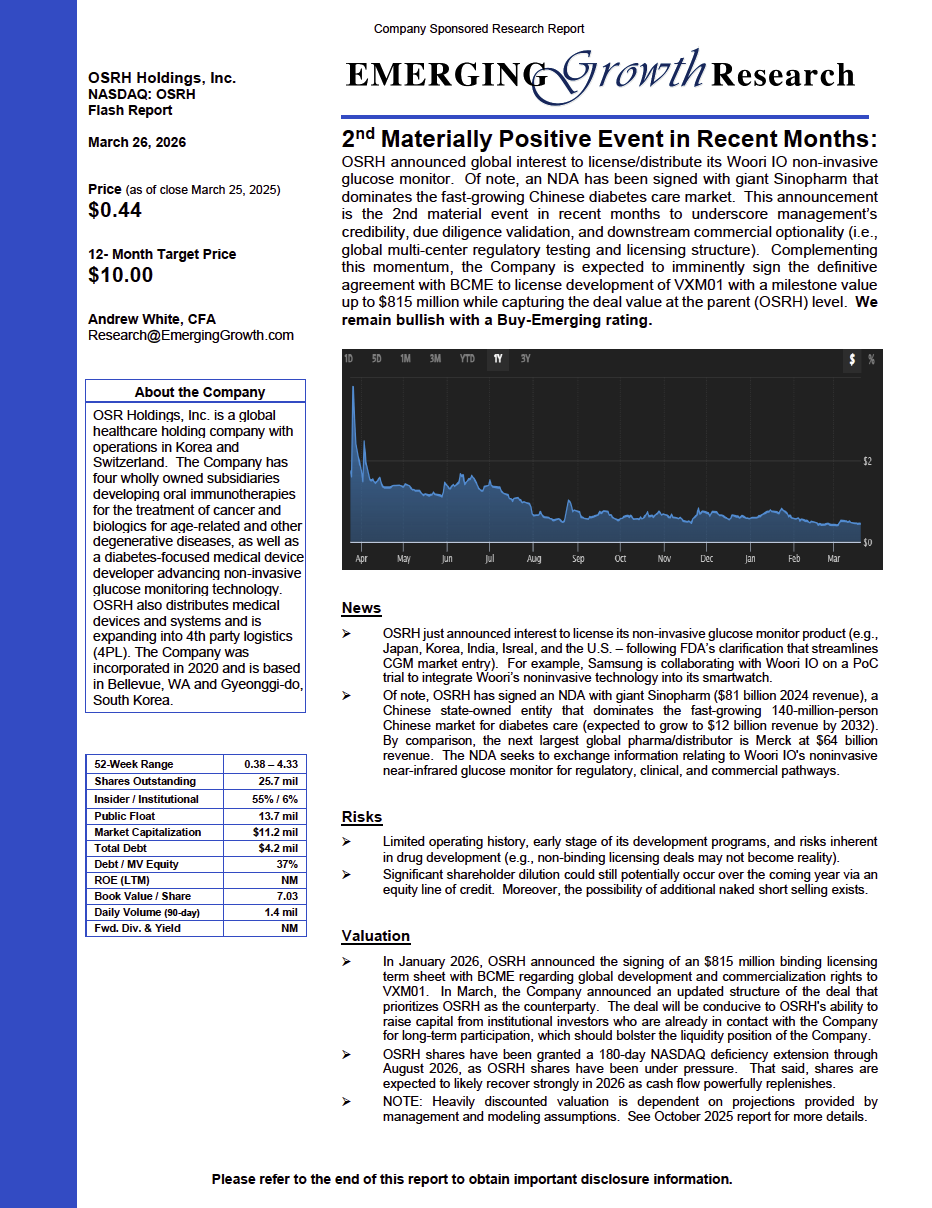

OSR Holdings, Inc. (NASDAQ: OSRH) Emerging Growth Research Report – March 26, 2026

2nd Materially Positive Event in Recent Months: OSRH announced global interest to license/distribute its Woori IO non-invasive glucose monitor. Of note, an NDA has been signed with giant Sinopharm that dominates the fast-growing Chinese diabetes care market. This announcement is the 2nd material event in recent months to underscore management’s credibility, due diligence validation, and downstream commercial optionality (i.e., global multi-center regulatory testing and licensing structure). Complementing this momentum, the Company is expected to imminently sign the definitive agreement with BCME to license development of VXM01 with a milestone value up to $815 million while capturing the deal value at the parent (OSRH) level.

Virtuix Holdings Inc. (NASDAQ: VTIX) Emerging Growth Research Report – March 6, 2026

Virtuix Holdings Inc. (VTIX) announced pleasing fiscal Q3:26 earnings, but shares sold off following its circa +60% price rise off lows. Trailing nine-month revenue through Dec-2024 was up +41% yoy, though fiscal Q3:26 (calendar Q4:25) yoy revenue declined vs. 2024 order backlog clearance. The important metric to focus on is new orders that were up +60% during December 2025 holiday yoy. The Company’s market-leading, patent-protected, full-body VR multi-use product growth strategy (consumer, enterprise, and defense) combined with recurring software licensing and gaming income plus several new positive developments (see below) bode well for even faster growth. Moreover, valuation is potentially discounted (Price/Sales calendar 2027E) to undervalued (DCF analysis), as 2027+ growth is expected to display a hockey stick profile. This condition is attractive for a growth company. Time for the long-term investment case to shine.

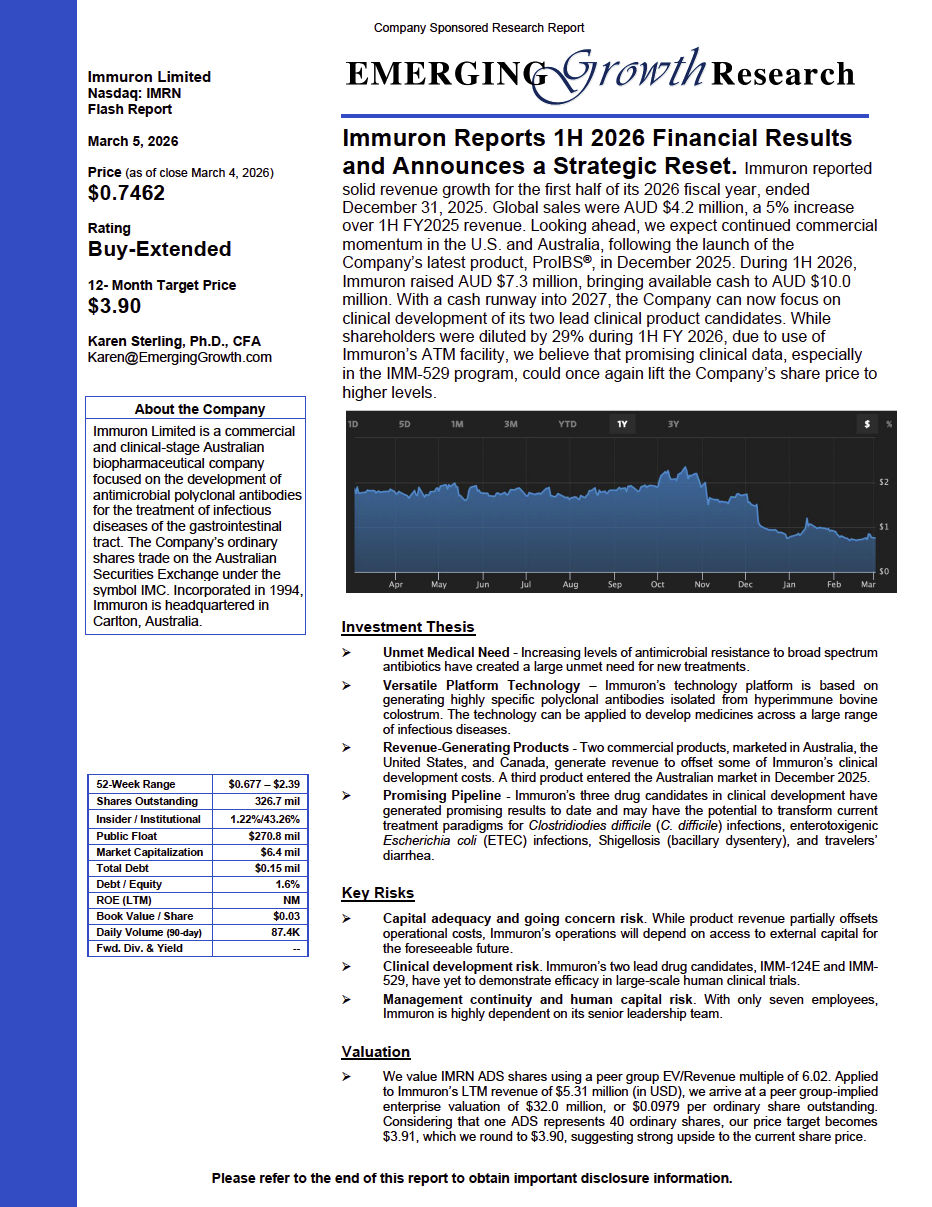

Immuron Limited (NASDAQ: IMRN) (ASX: IMC) Emerging Growth Research Report – March 5, 2026

Immuron Reports 1H 2026 Financial Results and Announces a Strategic Reset. Immuron reported solid revenue growth for the first half of its 2026 fiscal year, ended December 31, 2025. Global sales were AUD $4.2 million, a 5% increase over 1H FY2025 revenue. Looking ahead, we expect continued commercial momentum in the U.S. and Australia, following the launch of the Company’s latest product, ProIBS®, in December 2025. During 1H 2026, Immuron raised AUD $7.3 million, bringing available cash to AUD $10.0 million. With a cash runway into 2027, the Company can now focus on clinical development of its two lead clinical product candidates.

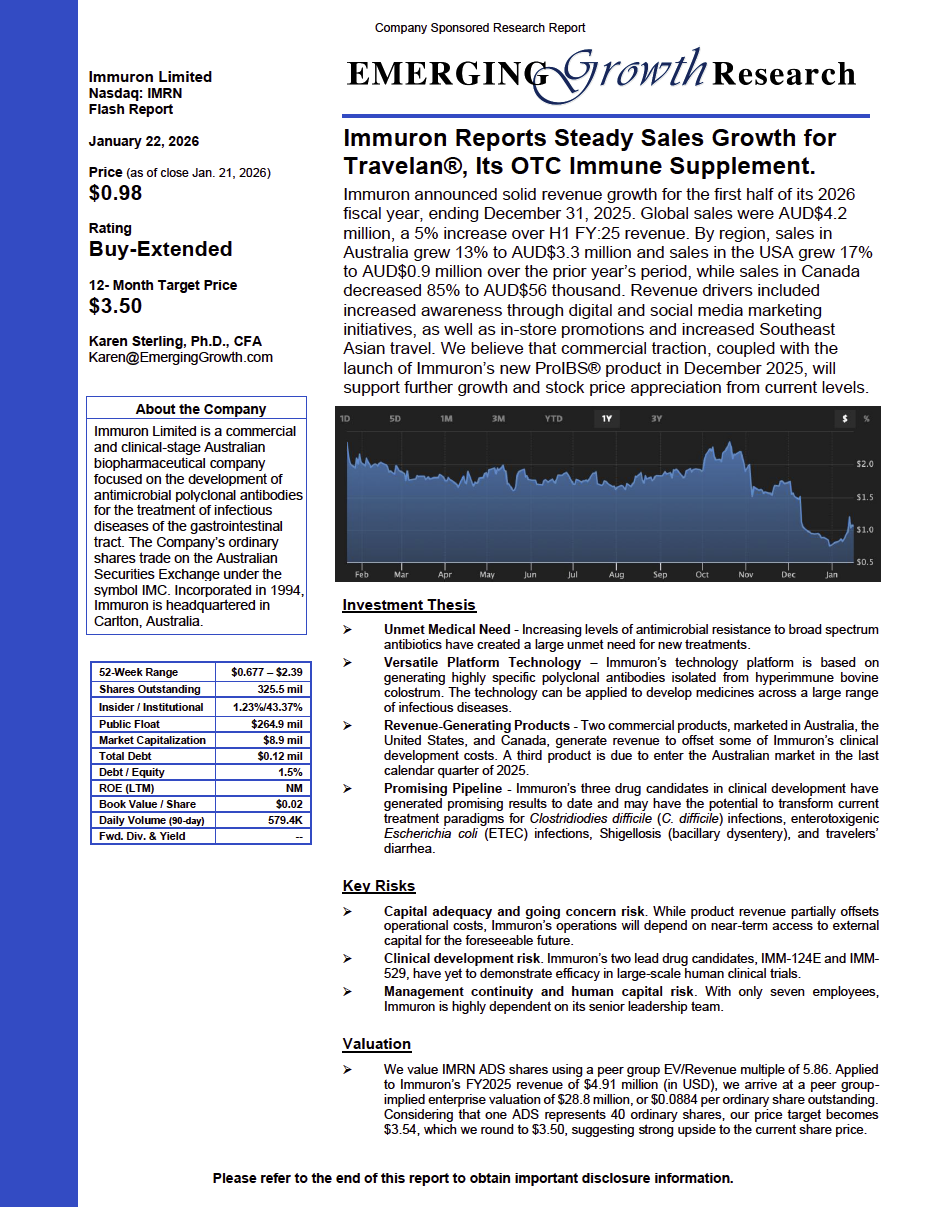

Immuron Limited (NASDAQ: IMRN) (ASX: IMC) Emerging Growth Research Report – January 22, 2026

Immuron Reports Steady Sales Growth for Travelan®, Its OTC Immune Supplement. Immuron announced solid revenue growth for the first half of its 2026 fiscal year, ending December 31, 2025. Global sales were AUD$4.2 million, a 5% increase over H1 FY:25 revenue. By region, sales in Australia grew 13% to AUD$3.3 million and sales in the USA grew 17% to AUD$0.9 million over the prior year’s period, while sales in Canada decreased 85% to AUD$56 thousand. Revenue drivers included increased awareness through digital and social media marketing initiatives, as well as in-store promotions and increased Southeast Asian travel. We believe that commercial traction, coupled with the launch of Immuron’s new ProIBS® product in December 2025, will support further growth and stock price appreciation from current levels.